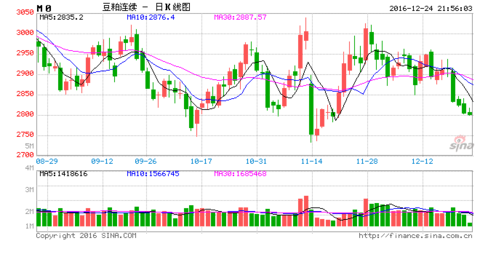

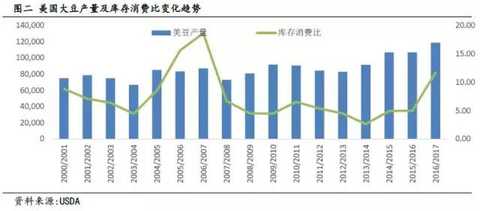

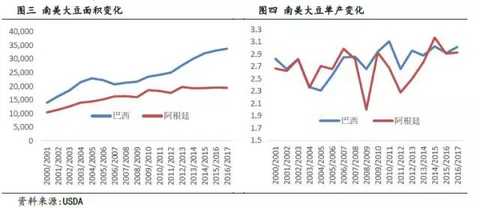

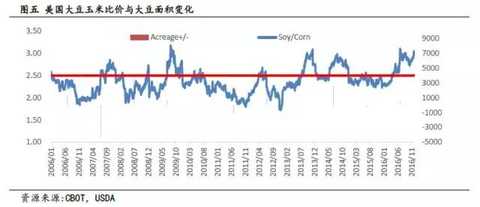

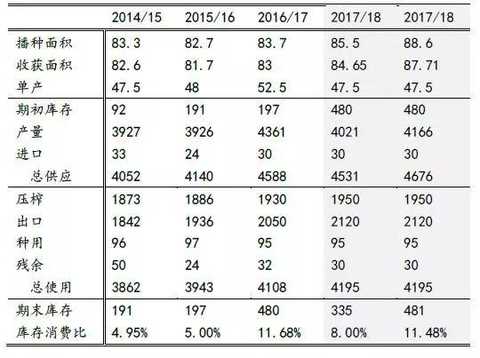

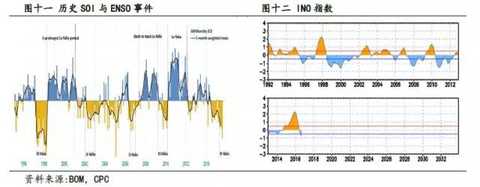

Hot spot funds flow to thousands of stocks to evaluate stocks to diagnose the latest rating simulation transaction Client The fund manager's mouse warehouse, said that the capital preservation has become a huge loss, and the fund is pitted to the [fund exposure station]! The credit card was stolen without any reason, the bank deposit became insurance, and the financial management was cheated, please poke [Financial Exposure Desk]! Original title: 2017 Outlook: Soybean meal is not pessimistic in the future In 2016/17, the global soybean stock consumption ratio was 24.8%, which was only slightly increased from the previous year, and it was significantly better than the 2014/15 inventory consumption ratio of 26.1%, which is the most stressful supply and demand pressure in this bear market. The 2016/17 US The domestic inventory consumption ratio is 11.7%, the bottom interval is 930-940. When the most pessimistic last year, the estimated inventory consumption ratio is more than 13%. The bottom interval is 840-850. The balance table of the US soybean loose has been reflected in the price trajectory to a large extent. The supply pressure in South America is relatively limited. The export pace of US soybeans is very fast, which is enough to become the main factor for the rebound of US soybeans in the fourth quarter. The uncertainty of the cycle weather in La Nina determines that the potential for global soybean yield rise is limited. The domestic pig industry has begun to recover and supports soybean meal consumption. It is estimated that China's soybean imports in 2016/17 will increase by 2-3%. The late rise space of the US soybean is greater than the downside space. Under the premise that there is no substantial problem in the weather in South America, the US soybean futures price still has a certain risk of falling back, and will reach a stage low in January and February, but it is expected to fall below the 950 line. If there is weather hype in South America, it is not possible to rule out the possibility of rushing to the 1200 line again. After the second quarter of 2017, the market focus will be transferred to the US soybeans. The return of the yield will be offset by the expected increase in the area, and the uncertainty of the weather makes the US soybeans easy to rise and fall. Domestic soybean meal should be boosted by the recovery of pigs, RMB depreciation and inflation expectations, and should be treated more in the general direction. In the first quarter, palm oil production recovery is limited, soybeans have pressure on South American listing, oil-to-oil ratio will remain strong, and may fall after the first quarter. I. 2016 market review For the commodity futures market, 2016 is a less calm year. The capital inflow under the background of the supply-side reform and the asset shortage led to the ups and downs of commodity futures, and the increase in coke from the low point of last year to the high point of this year reached 267%, which is indeed the leader of commodities. Relatively speaking, under the scenario of de-stocking cycle and overall good weather conditions, agricultural products are relatively dull and the light is mostly covered by industrial products. However, if you focus your attention on each single agricultural product, you will find that the agricultural products are actually dark, and the soybean meal and vegetable meal are the unstable elements. In 2016, domestic soybean meal increased sharply from the low level at the beginning of the year to a high point of more than 1,000 yuan / ton. Until the US Department of Agriculture released the report on the planting area at the end of June, the apes began to turn around and continued to fall to mid-October, after which the road to shocks and rebounds began. In general, the fluctuations in the bean curd in the past year were mainly dominated by the outer disk. Here, we will sort out several key stages and contradictions in the evolution of the US soybean and the intra-industry market in the past year. The rising stage: Since March, the US soybeans have risen out of the four-wave pulse relay. First, under the pressure of high-yield and listing in South America, investment funds have allocated a large number of soybean shorts. However, after repeatedly testing the lows around 850 cents and failing to break through, the funds have risen to patience, driven by the appreciation of the Brazilian real. Large-scale short-selling, the US soybeans began to rise in the first wave. After April, the main soybean producing areas in Argentina ushered in continuous rainfall, causing some production damage and delays in harvesting, and the funds began to add long positions. After the release of the supply and demand report in May, the US Department of Agriculture's old stocks, new crop production and carry-over stocks were lower than market expectations, and once again ignited the market's enthusiasm, the US soybean prices also rose to the next level. In June, affected by the high temperature concerns in the main producing areas, the US soybeans rose again and reached a stage high. Fallback stage: In late June, as the weather forecast shows that high temperature and dry weather are expected to be alleviated, and the area of ​​the planting area is reported to increase the area data, the US soybeans began to fall back, and the subsequent good rate of crops has been very good, making the market expectation of yields successively. The increase has increased the pressure on the production of Meidou. Concussion rebound stage: After the price fell to a lower position, the high-yield expectations have been largely digested. Then the US soybean weekly export data performed well, and the shipment progress was faster than in previous years. The US soybeans formed certain support and the price began to appear. Rebound. Second, international soybean supply and demand analysis 2.116/17 global soybean supply and demand is loose, but new pressure is limited According to the USDA's estimate, US soybean production in 2016/17 was 119 million tons, an increase of 11% over the previous year, exports reached 55.79 million tons, an increase of 5.89%, and crushing was 52.53 million tons, an increase of 2.32%. The increase in output led to a growth in demand, but the increase in demand was lower than the increase in output, which resulted in a turnover of 13.07 million tons at the end of the period, which was more than 10 million tons last time in 2007/08. The inventory-to-consumption ratio reached 11.7%, the highest level in the past 10 years. . South America , due to the soaring corn prices in Brazil in the first half of 2016, stimulating some farmers to switch to corn, coupled with the most serious economic recession in the past decade, led to credit tightening. This year's soybean area growth rate is the smallest in recent years, estimated at 3360-33.9 million. Hectare. On the Argentine side, in 2015, the new president, Markri, canceled the export tariff on corn and wheat, lowered the export tariff of soybeans by 5% to 30%, and plans to further reduce soybean tariffs in the future. However, in early October, Mark said that in 2016 and 2017, soybean export tariffs will not be lowered, and from January 2018 to December 2019, tariffs will be lowered by 0.5% per month. This will have a greater impact on farmers in northern Argentina, because of lower yields, higher planting costs, and higher costs for transporting soybeans to ports. Farmers plant in the northern region at current costs and 30% tariffs. Soybeans will be unprofitable. Dr. Kordonne, an agricultural expert, expects an increase of 800,000 hectares of corn in Argentina and 600,000 hectares of soybeans. We believe that the contraction of the area of ​​Argentina is certain, and the final planting area is roughly between 19,050,980,000 hectares. Considering the limited increase in soybean plantings in the new season in South America, the key to future supply is to maintain good yields. According to estimates by the US Department of Agriculture, South America's G2 soybean production will reach 159 million tons, an increase of 5.7 million tons from the previous year. Taken together, global soybean production increased by 22.89 million tons in 2016/17, but demand also increased. The final carry-over stock is expected to increase by 4.45 million tons, and inventory consumption is 24.8%, a slight increase from 24.4% in the previous year. 2.3 2017/18 US soybean supply and demand outlook Since the beginning of this year, the overall trend of the US soybeans is stronger than that of corn, so that the soybean corn price will remain above the normal level of 2.5 for most of the time. If this price relationship continues to be maintained, it will stimulate the next season of US soybean sowing, making the US soybean area Continue to increase in the next quarter. At the end of November, USDA expects US soybean plantings to increase to 85.5 million acres in 2017/18, while INFORMA is expected to increase to 88.6 million acres. In general, the probability of an increase in area in the next season is large, and the increase is expected to be between 2-6%. We use the USDA and INFORMA estimates and use the trend extrapolation method to estimate the next year's yield level and make a preliminary estimate of the 2017/18 US soybean supply and demand balance. It can be seen that when the weather returns to the general level and the US soybean yield level drops to the trend level of 47.5 pu/acre, the US soybean production will decline and the inventory consumption ratio will also shrink. However, the future situation is relatively large, but based on the estimation of the area of ​​the existing mainstream institutions, we do not see a clear prospect of a significant increase in production. Third, domestic supply and demand analysis Since 2013, with the de-capacity of the domestic pig breeding industry, feed production has also entered a new stage, and the output growth rate has a clear turning point. As the rapid growth of the industry's dividends disappeared, competition among feed companies intensified, and the industry also ushered in a round of reshuffle. According to statistics, from 2013 to 2015, the number of domestic feed processing enterprises was reduced to 6,764. According to the “13th Five-Year Development Plan for the National Feed Industry†issued by the Ministry of Agriculture in late October, by 2020, the expected output of meat, milk and aquaculture products in the country will be 90 million tons, 41 million tons and 52.4 million tons respectively. , respectively, increased by 4.3%, 5.9% and 6% compared with 2015, and the expected output of poultry eggs is 30 million tons, which is basically the same as in 2015. From now to 2020, it is necessary to increase the consumption of 16 million tons of compound feed, with an annual growth of about 4 million tons, a growth rate of 1.9%. The feed rate of meat and poultry industry feeds exceeds 90%, and the annual feed penetration rate of pigs with more than 50 pigs per year is 75%. In the next five years, feed utilization efficiency can be increased by more than 3%, and about 6 million tons of compound feed can be saved. In general, the “13th Five-Year Plan†indicates the direction of the supply-side structural reform of the feed industry that needs to enter the low-speed growth period, and also reflects the relatively stable stage of feed demand in the future. Look at the situation of domestic aquaculture in the past year. Domestic pig profit has remained at a high level in 2016, which has created a certain stimulus for downstream aquaculture enterprises. In our industry research, we learned that farmers in some parts of the country have begun to fill the gilts, but due to the increase in environmental standards, the extent of their expansion is not very radical. Overall, we believe that there will be a certain rebound in the number of live pigs next year, making the demand for pig feed next year a relatively optimistic expectation. Laying hens are in a good profit state for most of 2016, and it is expected that egg poultry will continue to maintain a better state next year. On the whole, we believe that the feed as a whole will remain in a stable and increasing state next year, with an overall increase of around 1-2%. 3.2 Soybean imports keep growing Domestically, due to the high profit of pig breeding in the first half of the year, some farmers have a greater mentality and increased the proportion of soybean meal in the ingredients, which boosted the demand for soybean meal and made the demand for soybean meal still poor. -6% growth. According to customs statistics, China imported 83.23 million tons of soybeans in 2015/16, an increase of 4.87 million tons. In the same period, rapeseed imports decreased by 580,000 tons, and DDGS imports decreased by 1.37 million tons. Considering that domestic rapeseed is also reduced, the supply of hybrids is shrinking in 2015/16, and the gap in making up the miscellaneous is also a source of demand for soybean meal. Looking forward to the next year, domestic rapeseed and soybeans will see a recovery growth, but considering their own base is too small, the absolute value of the increase is expected to be relatively limited. On the DDGS side, on September 23, 2016, the Ministry of Commerce announced the preliminary ruling of the anti-dumping investigation. It initially ruled that dumping of imported dry corn distiller's grains (DDGs) originating in the United States would impose 33.8% on dry corn distiller's grains from several US companies. Anti-dumping duties and immediate effect. On September 28, the Ministry of Commerce continued to announce the results of the preliminary ruling of the countervailing investigation. It initially ruled that there was subsidy for imported dry corn distiller's grains originating in the United States. The domestic dry corn distiller's grains industry suffered substantial damage and there was a gap between subsidies and substantial damage. Causality, and decided to implement temporary countervailing measures in the form of temporary countervailing duty deposits for imported dry corn distiller's grains products originating in the United States. According to the ruling, since September 30, 2016, importers importing dry corn distiller's grains originating in the United States should be based on the adjudication rate (10.0%-10.7%) determined by the ruling to China. The Customs of the People's Republic of China provides the corresponding temporary countervailing duty deposit. From the current situation, after the anti-dumping and countervailing duties are imposed, DDGS will be basically unprofitable. It is expected that DDGS imports will be significantly reduced next year. On the whole, we will continue to increase the growth of domestic soybean imports next year, but considering the recovery of oil production and the slowdown in the growth of farming demand, the growth rate will also be at a relatively low level, with a preliminary estimate of growth of 2-3. %between. Fourth, the potential variable From the development pattern of domestic aquaculture and feed industry, although we believe that domestic feed demand will increase in the next year, and demand for soybean meal will increase, domestic feed aquaculture has entered a relatively stable stage, especially domestic trade. Under the background that the beans have been largely withdrawn and the market has returned to the industrial demand, there are not many stories about the Chinese demand story. The next year's potential contradictions are still on the supply side, which is also the place to focus on in the future. 4.1 Uncertainty of yields under the “La Nina†cycle With the departure of El Niño, the market is paying more and more attention to the development of La Nina. Earlier, the monitoring of the Australian Meteorological Administration (BOM) showed that the Southern Oscillation Index (SOI) turned to a downward position after reaching a high of 13.5 in September, and was operating in a negative range in October and November. In general, the SOI continues to exceed 7 to determine the La Niña event. At present, seawater in the central Pacific has begun to warm up, and the negative return range of SOI has adversely affected La Nina. However, the NOAA November report showed that La Nina's probability of maintaining this winter is 55%, which means that La Nina can not be completely ruled out. According to historical statistics, the general La Niña year, the global soybean production area will be affected, mainly because La Nina affects local precipitation, of which Argentina's infrastructure is poor and affected the most. From the current expectation, this La Nina is a weak La Niña event, which has less impact on South America. However, in the past 20 years, La Nina generally lasts for a long time. Whether La Nina will strengthen and influence the US soybean production next year is still unknown. 4.2 Does the US soybean export exceed expectations? Due to the rapid sales of Brazilian soybeans, Argentina's production was damaged, South American soybeans decreased in the early 2016/17 period, and the United States became the mainstay of global soybean supply. Since the beginning of the new market year, US soybean exports have maintained a very good rhythm. According to USDA data, as of November 17, US soybean export shipments totaled 21.81 million tons, reaching 39% of annual export estimates, the highest level in the past 10 years; export orders were 40.37 million tons, which is an annual export forecast. 72%, the fifth highest level in the past 10 years. US soybean exports maintain a fast pace to meet international demand, which is a normal reaction in the context of the current US monopoly supply. However, buyers are more optimistic about South American future supply expectations, and are not particularly eager to purchase more long-term orders in the United States. This puts higher demands on the certainty of supply in South America. As long as the South American soybean growth period is worried about the loss of production, it is easy for the US soybeans to get funding speculation, which will make it difficult for the US soybeans to rise before the South American production is determined. The basis of the fall. However, the weather in South America is generally unimportant, and the output prospects are temporarily unaffected. The US soybeans rose above 1050. The market began to talk about China's cancellation of some orders, which caused the pressure on the top to increase. Overall, the direction of the future US soybeans will depend to a large extent on the strength and timing of the recovery of South American soybeans. Before the South American output has no substantial threat, the US soybeans will maintain a pressure and a bottom-down shock pattern. V. Analysis of investment opportunities From the perspective of CBOT soybean fund positions, since the global soybean entered the bear market in the second half of the year, the proportion of net positions held by fund positions has been declining. At the lowest level, it has become more than 10% of the net position, but as the bear market continues into 2016, In the bean market, there have been some bullish stimuli such as the appreciation of the Real, the flood of Argentina, the unexpected increase in the yield of the US soybeans, and the weather concerns. The US soybeans have also emerged from a sharp upward trend. After the weather speculation was lifted and the yields continued to rise, the US soybean futures price began to fall, but in the process, the fund's net position has always maintained a relatively high net position. Fund holdings show that speculative funds are no longer so pessimistic for the future, which also creates a relatively bullish market atmosphere. Combined with the previous analysis, we tend to think that the US bear cycle in this round has ended, and the upward space in the later period is larger than the downward space. The main reasons are as follows: 1. From the perspective of the annual supply and demand balance sheet, the 2016/17 soybean stock consumption ratio was 24.8%, which was lower than the 2014/15 high of 26.1% in the current bear market cycle. Beans provide a stable external environment; 2. CBOT trades the balance sheet of US soybeans. In retrospect, the current US supply and demand balance table gives an inventory consumption ratio of 11.7%, and the bottom range is between 930 and 940. The bottom section of 840-850 last year corresponds to more than 13% expected inventory consumption ratio, and the estimated inventory consumption ratio has not exceeded 12% so far this year. The bottom of the futures price rise reflects the expected change in supply and demand; 3. According to our analysis of the supply and demand of US soybeans in the next market year, we believe that even if the US soybean area increases in the second half of the year, it is difficult to further increase the US soybean stocks consumption ratio under the trend of trend yield. On the whole, we believe that there is still a certain risk of falling back in the US soybean futures price under the premise that there is no substantial problem in the weather in South America, and will reach a stage low in January and February, but it is expected to fall below 950. A line. If there is weather hype in South America, it is not possible to rule out the possibility of rushing to the 1200 line again. After the second quarter of next year, the market focus will be transferred to the US soybeans. The return of the yield will be offset by the expected increase in the area, and the uncertainty of the weather makes the US soybeans easy to rise and fall. 5.2 The overall thinking of soybean meal Since mid-November 2016, the domestic soybean meal spot price performance is very strong, which is not commensurate with the relatively loose and loose background of global soybean supply. The reason is the staged supply and demand mismatch. At the beginning of September and October, domestic imports of soybeans arrived in Hong Kong in a lesser stage, and the spot was tight. However, it is widely expected in the industry that after the arrival of new soybeans in Hong Kong, there will be a significant increase in the arrival of Hong Kong, forming a short-term expectation, downstream traders and feed. The plant also maintains a low inventory level. However, it was later discovered that the cargo was actually delayed in Hong Kong. In November, the arrival of soybeans in Hong Kong did not rise as expected, which made the supply of soybean meal not keep up, and the downstream passive replenishment bank pushed up the spot. In addition, after the domestic trucks are limited in load, the capacity is tight, and the downstream is expected to become more tight as the Spring Festival approaches. Therefore, the stocking period is advanced, which makes the spot price further strengthen, which makes the 1-5 spread rise from 60 to 184 yuan. The corresponding spot continued to remain firm for the January basis, and the mainstream region remained at 300-450. Overall, the tight spot of soybean meal is expected to ease at the end of December, but due to the large-scale contract sales of oil plants, it is not expected to form greater pressure. Thanks to the increase in the spot price of domestic soybean meal, the profit of imported soybean crush has also rebounded to a higher level. We expect that there will be some pressure on the domestic soybean meal after the Spring Festival. There may be a chance of a period of May in May, but this time. Depending on the ship's schedule data and safety margins, it is recommended to keep track of it. From the perspective of the larger cycle, from 2015 to the first quarter of 2016, the domestic soybean meal spot premium maintained a narrow range of oscillations in a low range. However, from the second quarter of this year, the overall spot price showed an upward trend, and the domestic soybean meal basis began to rise. This aspect has the reason for the cost increase, on the other hand, the profit of pig breeding is better, the farmers are pressing the bar, and the quality of protein is increased. We expect that with the cyclical recovery of domestic pig breeding industry, the demand for soybean meal will be cautiously optimistic next year. The pattern of spot premium will continue and may remain at a high position, but it is difficult to exceed the high point since the fourth quarter of 2016. The inter-period spread will mainly reflect In the staged arrival rhythm and long-term theme speculation. On the one hand, the domestic soybean meal will continue to follow the US soybeans in the general direction, and the stage strength will be dominated by the disk. Considering the depreciation of the renminbi and inflation expectations, coupled with the recovery of domestic farming, the direction of soybean meal should be more inclined. 5.3 Oil to oil ratio From the historical review point of view, the cost factor of the rise of the US soybean is mostly reflected in the domestic soybean meal, so the rise of the US soybean often corresponds to the weakening of the domestic oil-to-oil ratio. In 2015, Petronas's ratio was also full of twists and turns. First, the strength of palm oil under the influence of El Niño led the oil to rise. After April, as the US soybeans went higher and palm oil production was expected to recover, the oil rafts fell again until the end of June. With the arrival of the peak demand season in the second half of the year, the recovery of palm oil production in Southeast Asia is less than expected, and the increase in US soybean yields and the fall in US soybean prices, oil prices are pushing higher than the other, but they have not yet exceeded this year's high. In 2017, from the global vegetable oil stock consumption ratio, it dropped to a lower position, which provided a background for oil. Although palm oil in Southeast Asia will increase production, it is expected that palm oil recovery will be limited before the first quarter of next year, while the Malaysian and Indonesian biodiesel policies will boost demand and the US EPA will increase the proportion of biodiesel mandatory. The overall performance of the oil will also be in a strong pattern. At least until the end of the first quarter of 2017, the oil will not see too much pressure. If the weather in South America is not a big problem, the whole oil ratio will still maintain a strong pattern. After the first quarter, depending on the recovery of palm oil and the expected new crops of US soybeans, it is more likely that oil stagnation will weaken. Zhongcai Futures Research Institute Enter [Sina Finance and Economics Unit] Discussion

Polyester yarns are obtained by melt spinning from a polymeric melt at 265 °C. In polyester yarns, crystalline and amorphous areas exist. They are a thermoplastic material. The chains have a zig-zag structure and are linked to each other by Van-der-Waals connections.

Polyester yarns create garments that keep their shape and are generally machine-washable when on their own, which makes it a great selection for baby projects. When used in a Yarn blend, polyester adds durability and structural stability to your projects. Polyester and polyester blend yarns are a great choice for outerwear garment and high use accessories. Spun Yarn Polyester Yarn,Polyester Spun Yarn 30/1,20/1 Ring Spun Yarn,Polyester Yarn Antistatic,Polyester Acrylic Yarn NINGBO S.DERONS IMPORT AND EXPORT CO.,LTD. , https://www.sderonsyarn.com

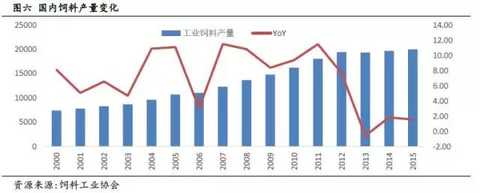

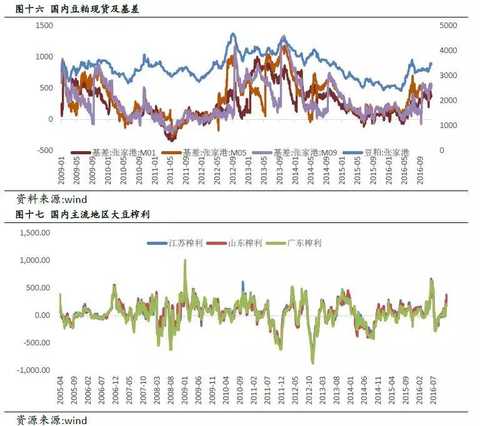

3.1 Domestic feed production grows steadily

5.1CBOT soybean up space is larger than down space